[ad_1]

At the identical time of TensorFlow’s increase, foreshadowing what was but to arrive in open resource AI, company software package went by way of an open supply licensing disaster. Largely thanks to AWS, which experienced mastered the craft of having open up source infrastructure jobs and making commercial services all over them, numerous open up supply tasks exchanged their permissible licenses for “Copyleft” or “ShareAlike” (SA) solutions.

Not all open supply is designed equivalent. Permissible licenses (like Apache 2. or MIT) allow any person to just take an open resource undertaking and establish a professional company all-around it. “Copyleft” licenses (like GPL), equivalent to Inventive Common’s “ShareAlike” phrases, are a single way to secure towards this. They are in some cases referred to as a “poison pill”, mainly because they need any spinoff item to be certified the same way. If AWS released a provider primarily based on an open up resource challenge with a “Copyleft” license, the AWS assistance itself have to be open sourced under the exact license.

So, partially in response to aggressive cloud providers, the company creators and maintainers of open up source initiatives like MongoDB and Redis switched up their licenses to much less permissible solutions. This led to a unpleasant but entertaining back again-and-forth among AWS and these companies on the concepts and deserves of open up supply, which has due to the fact calmed down a bit.

Take note that this transform in licensing experienced a deceptive effect on the open up supply ecosystem: There are continue to a large amount of new open up resource projects remaining announced, but the licensing implications on what can and are unable to be completed with all those initiatives are much more intricate than most people today know.

At this issue you ought to be asking yourself: If the company maintainers of open resource infrastructure projects realized that other people were being reaping additional of the industrial rewards than on their own, should not the similar be going on with AI? Is not this an even even larger offer for open up resource AI designs, which hold the aggregate price of compute and facts that went into creating them? The answers are: Yes and sure.

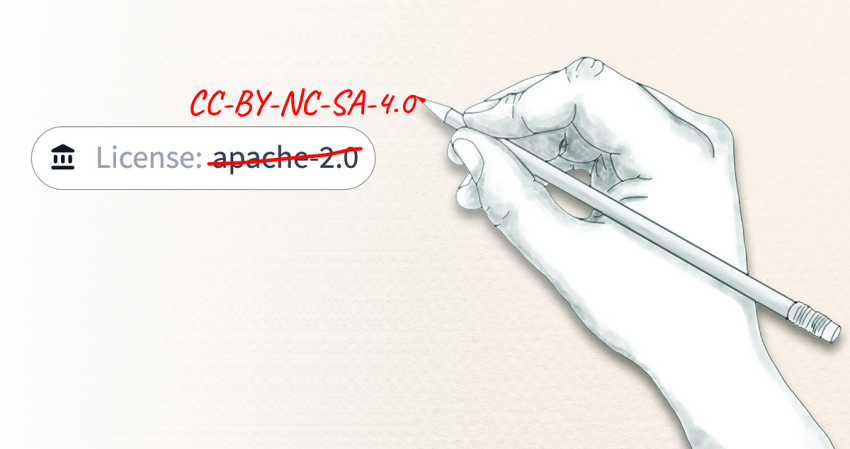

Even though there appears to be a Robin Hood-esque motion close to open up source AI, the data is pointing in a diverse direction. Substantial firms like Microsoft are switching licensing of some of their most preferred designs from permissible to non-commercial (NC) licenses, and Meta has started out to use non-commercial licenses for all of their current open up source initiatives (MMS, ImageBind, DINOv2 are all CC-BY-NC 4. and LLAMA is GPL 3.). Even popular initiatives from universities like Stanford’s Alpaca are only accredited for non-industrial use (inherited by the non-permissible attributes of the dataset they applied). Full businesses alter their enterprise products in order to protect their IP and rid by themselves of the obligation to open resource as aspect of their mission — don’t forget when a modest non-earnings termed OpenAI reworked itself into a capped-gain? Discover that GPT2 was open up sourced, but GPT3.5 or GPT4 were being not?

Much more commonly talking, the craze in the direction of less permissible licenses in AI, whilst opaque, is recognizable. Below is an investigation of product licenses on Hugging Facial area. The share of permissible licenses (like Apache, MIT, or BSD) has been on a persistent drop due to the fact mid 2022, although non-permissible licenses (like GPL) or restrictive licenses (like OpenRAIL) are turning into a lot more common.

To make items even worse, the modern frenzy around significant language styles (LLMs) has even more muddied the waters. Hugging Deal with maintains an “Open LLM Leaderboard” which aims to emphasize “the authentic progress that is becoming designed by the open-source neighborhood”. To be honest, all of the designs on the board are in truth open source. Even so, a closer glimpse reveals that nearly none are licensed for industrial use*.

*In between the creating of this write-up and its publication, the license for Falcon versions improved to the permissible Apache 2. license. The total observation is still legitimate.

If just about anything, the Open LLM Leaderboard highlights that innovation from massive tech (LLaMA was open up sourced by Meta with a non-commercial license) dominates all other open up supply efforts. The more substantial trouble is that these by-product models are not as forthcoming about their licenses. Virtually none declare their license explicitly, and you have to do your possess exploration to discover out that the designs and info they are primarily based on really don’t permit for professional use.

There is a lot of virtue-signaling in the community, largely by effectively-meaning business owners and VCs who hope that there is a upcoming that is not dominated by OpenAI, Google, and a handful of some others. It is not clear why AI products must be open up sourced — they represent hard-earned intellectual house that providers establish above decades, expending billions on compute, facts acquisition, and talent. Businesses would be defrauding their shareholders if they just gave anything absent for free.

“If I could spend in an ETF for IP legal professionals I would.”

The development to non-permissible licenses in open up source AI seems obvious. Nonetheless, the too much to handle quantity of information fails to level out that the cumulative profit of this work accrues nearly fully to academics and hobbyists. Buyers and executives alike must be much more knowledgeable of the implications and exercise more care. I have a potent feeling that most startups in the rising LLM cotton industry are making on prime of non-commercially accredited know-how. If I could devote in an ETF for IP lawyers I would.

My prediction is that the price seize for AI (especially for the hottest era of substantial generative designs) will search related to other innovations that have to have important money investment decision and accumulation of specialised expertise, like cloud computing platforms or working units. A couple important players will arise that offer the AI basis to the relaxation of the ecosystem. There will even now be ample space for a layer of startups on major of that foundation, but just as there are no open resource assignments dethroning AWS, I consider it quite not likely that the open supply community will produce a major competitor to OpenAI’s GPT and what ever arrives subsequent.

[ad_2]

Resource hyperlink